I have thoroughly enjoyed studying Digital Business Models this term. The module is unique in that it is almost exclusively taught online. Moreover, the week-by-week subject content covers a range of topics that are both useful and relevant for society, business and the workplace going forward.

The first couple of weeks saw our learning temporarily shifted onto a popular MOOC platform, Future Learn. The site’s smooth and intuitive interface enhanced usability and accessibility, while its comment sections enabled lively and thought-provoking discussions to be had. The topics covered related to the future of work featuring trends such as AI, machine learning, amplified individuals, and much more. It was fascinating and enlightening to read and understand the opinions of others on these issues.

The future of work was also the topic of our first assessed blogpost where we had to assess the impact of the digital economy on a chosen job role. I selected the retail banker. I explored the blogs of my peers and commented on Sabine’s PR & Communications blog as well as Nicolette’s one on Marketing (see below).

Midway through the term, the module examined the rise of the “sharing” and “circular” economies, new business models, and the impact of digital disruption. From individual study and reviewing comments, I acquired a proper understanding of the theory behind “sharing” and “circular” economies as well as the concomitant fantastic business opportunities. With regards to new business models, I contributed Spotify as a business which makes use of SMAC.

However, it was only by reading the examples of companies, posted by my peers, that I realised how pervasive and disruptive these latest technologies are.

Our second assessed blogpost built on this and required us to critique the digital business model of a chosen company. I opted for Amazon whose business is almost exclusively online and has experienced phenomenal growth as a result. I found Ellis’s blog on “challenger” banks particularly interesting as well as Kirstyn’s on the rise of Airbnb and so, decided to comment on both (see below).

Towards the end of the module, we explored “Ethical Issues in the Digital World”. I think this is an important, but often neglected, topic which I raised in my comments on ELE:

It was good to read the thoughts of others on internet access inequalities and the rise of fake news as well as strategies to tackle these. The latter was particularly pertinent given the wave of disinformation online surrounding the current coronavirus pandemic.

Overall, reading, commenting, and participating in weekly module discussions has enriched my learning by providing differences in insight, perspective, and experience not typically gained through traditional classroom-style teaching.

Amazon’s digital business model has been instrumental to its success. Founded in 1994, Amazon has transformed from a marketplace for books into an internet giant. Its size has led to it being referred to as “one of the most influential economic and cultural forces in the world” (Jacoby, 2020). On its journey to achieving this remarkable growth and success, Amazon overhauled business models becoming an early adopter of an asset light, online alternative (Li, 2018, p.4). Its marketplace is exclusively online, known as e-commerce, and has since diversified into a range of goods far exceeding its original remit of a book-seller. More recently, in line with SMAC, Amazon has branched into cloud computing and digital streaming, and even the next level of digital transformation with artificial intelligence (Olenski, 2016, para.2). This blog will break down the key features of the company’s digital business model and explain how these have been so effective.

Online Shopping

Only Alibaba, its Chinese counterpart, can compete with Amazon in the scale and breadth of its online offering. Being online means the company completes all its sales and transactions through its website “Amazon.com” and does not own any “bricks and mortar” storefronts traditionally associated with major High Street names (Gray, 2019, para.2). Importantly for Amazon’s competitive advantage, this is how the company has functioned since its foundation. By contrast, other retailers have only made the shift towards online stores in the last 10 years. Therefore, not only has Amazon been leading the way in terms of consumer convenience from the very start, but it has also been able to undercut the prices of its competitors. This is because the company is not saddled with the overheads and labour costs which weigh on its rivals (Van Tulder, 2018, p.19). When online convenience, a diversified product range, and low prices are combined, a very appealing service is created.

Amazon Online Shop (LoveMoney, 2019)

Business Ecosystem

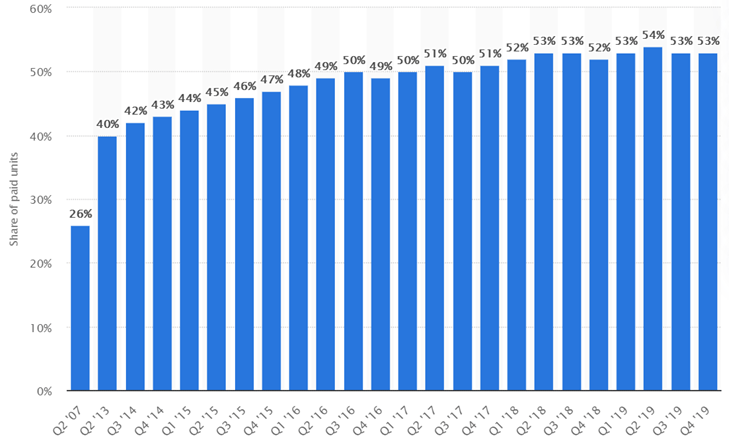

In addition to its direct sales, Amazon has also created a platform which allows for approved third party retailers to sell products to buyers. Amazon then takes a share of the sales price as commission. This is mutually beneficial for both parties as Amazon can avoid holding slow-moving inventory which may impact profits, while the third-party can increase their sales courtesy of the greater visibility and respectability conferred through Amazon’s brand image and search-engine-optimisation (SEO). This latter technological feature provides Amazon with powerful leverage with its supplier relationships. Evidence suggests this arrangement is becoming increasingly successful with the proportion of sales which third parties comprise soaring from a mere 3% in 1999 to as much as 53% today (Statista, 2019, para.1). This extra business and profitability is generated without any incremental cost or capital from Amazon.

Percentage of Amazon third-party sellers (Statista, 2019)

Despite managing an open ecosystem, Amazon does also operate a ‘closed’ platform in some areas. This refers to a company selling the customer an interdependent suite of products (Sherr & Totty, 2011, para.2). For example, a consumer may purchase a Kindle, however, they can only buy books from the Kindle Store. Equally, a consumer may appreciate the voice-functionality of an Alexa to play music, however, they are confined to Amazon Music. This technique is not unique with Apple utilising the App Store for its devices and Google with the Play Store.

Amazon Alexa and Music (Holt, 2018)

Subscription-based model

One of the common digital business models operated by companies is the subscription-based model and Amazon is no exception. Amazon Prime requires a monthly payment of £7.99 and in return provides you with next-day delivery for online orders, access to a wide variety of video and music streaming content, and a rotating selection of e-books for your Kindle. In an era of instant gratification, consumers increasingly want their purchases now and Amazon Prime does this. With over 150 million subscribers worldwide and revenue of over $15bn, Amazon’s subscription-based model has been a resounding success (Reisinger, 2020, para.5).

Freemium model

Freemium is a portmanteau of “free” and “premium”. While this may sound counter-intuitive, the term refers to the limited access a user will be given by a company to a subscription-based product or service. One example is this blogging platform WordPress which offers customers a basic version of its service with the option of upgrading to receive better features and capabilities. As a business technique, this is designed to give the consumer a flavour of a product/service with the ultimate goal of encouraging them to pay for the “premium” version. Amazon operates this model with regards to its music-streaming service. Prime gives the customer access to a selection of songs, however, an additional monthly fee is required to become “Unlimited”. Testament to its success, Amazon Music Unlimited now has 55 million subscribers putting it neck-and-neck with one of its major rivals, Apple (Bera, 2020, para.1).

Freemium (Quarton, 2015)

Conclusion

Amazon has made extraordinarily effective use of its digital business model, expanding into a myriad of industries, increasing its customer base, and disrupting established companies. Its reputation for convenience, best-in-class delivery and putting the customer first has been indispensable to this. Its digital disruption and success, putting customer service ahead of profitability, has resulted in a global market share for its platform model way beyond what was thought possible (Amazon, 2020, para.5).

The career path I have chosen for exploring the impact of the digital economy is retail banking. It is just over 30 years ago that First Direct (now part of HSBC) was launched as the UK’s first branchless bank. Its telephone-based customer service was designed to appeal to busy professionals but also began a change in the front line of retail banking. Now, the impact of digital disruption is transforming the consumer banking experience again. Omni-channel interaction is driving change for banks on the high street in a very similar way to the entire retail sector. So much so that a recent survey carried out by Accenture (2017, part 1, p.10) found that nearly 50% of consumers believe that traditional banks may not be necessary in the future. This figure is reinforced by the fact that nearly half of UK adults used mobile banking in 2018 in some way or other. Stephen Jones, CEO of UK Finance opined that “more and more customers are now opting for speed and convenience” (UK Finance, 2019, para.5).

The retail banking business model is having to adapt rapidly and this means the role of the front line retail banker is changing.

In terms of customer engagement, banks are becoming increasingly digitized. The network of branches across the country is shrinking fast with as many as 3,372 closures in the last four years (Briefing Paper, 2020, para.8). This is a pragmatic response to changing consumer demand which can be increasingly satisfied online. For instance, the emergence of internet banking available through an app on your digital device. Money transfers can be completed at the touch of a button, while I can pay in a cheque by simply taking a photo on my phone, whereas ten years ago my parents stood in the traditional lunch-time bank queue to engage with a bank teller to achieve the same outcome.

Lloyds Internet Banking App

While this maximises convenience for the customer and builds a sustainable consumer engagement platform, retail bankers are not having as many of the traditional face-to-face customer interactions of the past. Instead, the vast majority of interactions are increasingly self-serviced using digital solutions. The retail banker was already undergoing change from the traditional, transactional teller function towards trying to promote the bank’s services more actively. However, this is not always easy to do when there is a long queue building up. This has now changed with branches increasingly being remodelled to remove teller counters completely and replace them with fully integrated self-service machines, supported by “floating” customer advisers. These advisers have a very different role and skill set. They both train the non tech savvy, often older customer in how to use the self-service machines but are also sales professionals with the highest levels of training in the bank’s products. As customers become more comfortable with using self-service machines and online banking, the in-branch adviser roles will increasingly focus more on sales. Branches will therefore have fewer staff and with different skill sets.

Self-service machines

Having a personal presence is important for the traditional high street banks. Despite the emergence of new challenger banks in the sector, such as Monzo, Metro, Atom Bank etc, the market shares of the legacy banks have held up surprisingly well. There appears to be a residual loyalty and trust. It is therefore imperative that they continue to earn this trust through high levels of customer service and technological capability and convenience. However, this can be challenging as the major banks still have to wrestle with upgrades to their legacy systems and services outages as notably occurred with RBS and TSB in 2019 can be reputationally damaging.

There is a high demand for self-service by consumers today until it fails. AI powered chat bots are a useful way of dealing with basic banking problems (PWC, 2020, para.1). However, the personal touch still has a place in the retail banking environment especially where complexity is involved.

One interesting development last year was the introduction by HSBC of a 4 feet tall cute robot with a tablet attached to its chest which patrolled outside its 5th Avenue Manhattan branch. The purpose was to lure people into the branch, answer basic banking questions but also lead to higher value customer engagements for the in-branch advisers.

HSBC’s robot “Pepper”

In terms providing and training a workforce to perform at this new level, the banks have demonstrated a serious commitment to lifelong learning, acknowledging the benefits of developing the ‘amplified individual’. For example, it has become imperative for workers to “have the ability to maintain and renew the right skills through lifelong learning” (UK Government, 2017, part 1, p.6). Recognising this, PayPal recently started to offer on-demand, self-directed video learning to its employees. Consequently, in line with Ernest Wilson’s “third space thinking” (2016, p.1), retail bankers are showing initiative and taking ownership of their personal and career development.

In conclusion, AI is here to stay and it provides opportunities all round. For the customer, transactions can be done more quickly on-line or in branch, whilst human interaction remains available in branch; for banks it allows for a more profitable model without compromising customer service (deSouza, 2014, p.1); and for retail bankers, their roles become more skilled and fulfilling.